Spending Tracker with Notifications

Users expressed a need for improved visibility into spending habits. A spending tracker with real-time notifications was conceptualised to allow users, like Sarah and Abdul, to monitor expenses as they occurred, helping them avoid overspending.

Limited awareness of features and unclear balance tracking.

A simplified user interface (UI) for tracking daily expenses was proposed, with optional notifications for significant or unusual spending.

Customisable Budget Categories & Goals

Many users, particularly those managing complex household budgets or tight student finances, requested flexibility in categorising spending. This would enable the app to better align with unique financial situations.

Limited customization of budget categories and difficulty tracking category-specific spending.

Options for creating and labelling custom budget categories, setting specific monthly spending limits, and receiving alerts upon approaching set limits were included in the design.

Debt Repayment Tracker and Credit Improvement Tips

As debt management and credit building were essential for financial resilience, a tracker for loan repayments combined with credit score improvement tips was prioritised.

Difficulty understanding transaction summaries and a lack of tools for financial growth.

A dedicated section to track debt repayment schedules and display progress through a scoring system was proposed. Bud’s Open Banking API would support personalised tips for credit improvement based on financial behaviour.

Emergency Fund Setup Wizard

Users highlighted the need for guidance in building a savings buffer. An emergency fund setup wizard was conceptualised to help users allocate a portion of their budget toward emergency savings.

Absence of goal-setting tools and need for financial stability.

A guided flow for users to select an amount and timeline to reach a savings goal was outlined, with visual progress tracking and motivational reminders.

Long-Term Financial Goal Planner

The app would benefit from a tool that enabled users to set and track long-term goals, such as saving for retirement or major purchases, which was especially valuable for users at the Growth stage.

Absence of goal-setting tools and desire for long-term financial planning.

This feature included options to set individual financial goals and link accounts or savings options directly to these goals, with periodic reminders and projections to maintain motivation.

Investment Insights and High-Interest Savings Suggestions

Many users expressed a desire for an intuitive way to learn about investments. Integrating educational content and savings options was proposed to support users interested in wealth-building.

Desire for wealth-building knowledge and lack of educational resources.

A “Learn” section within the app was suggested to provide insights into investment basics and high-yield accounts, with tailored savings product recommendations.

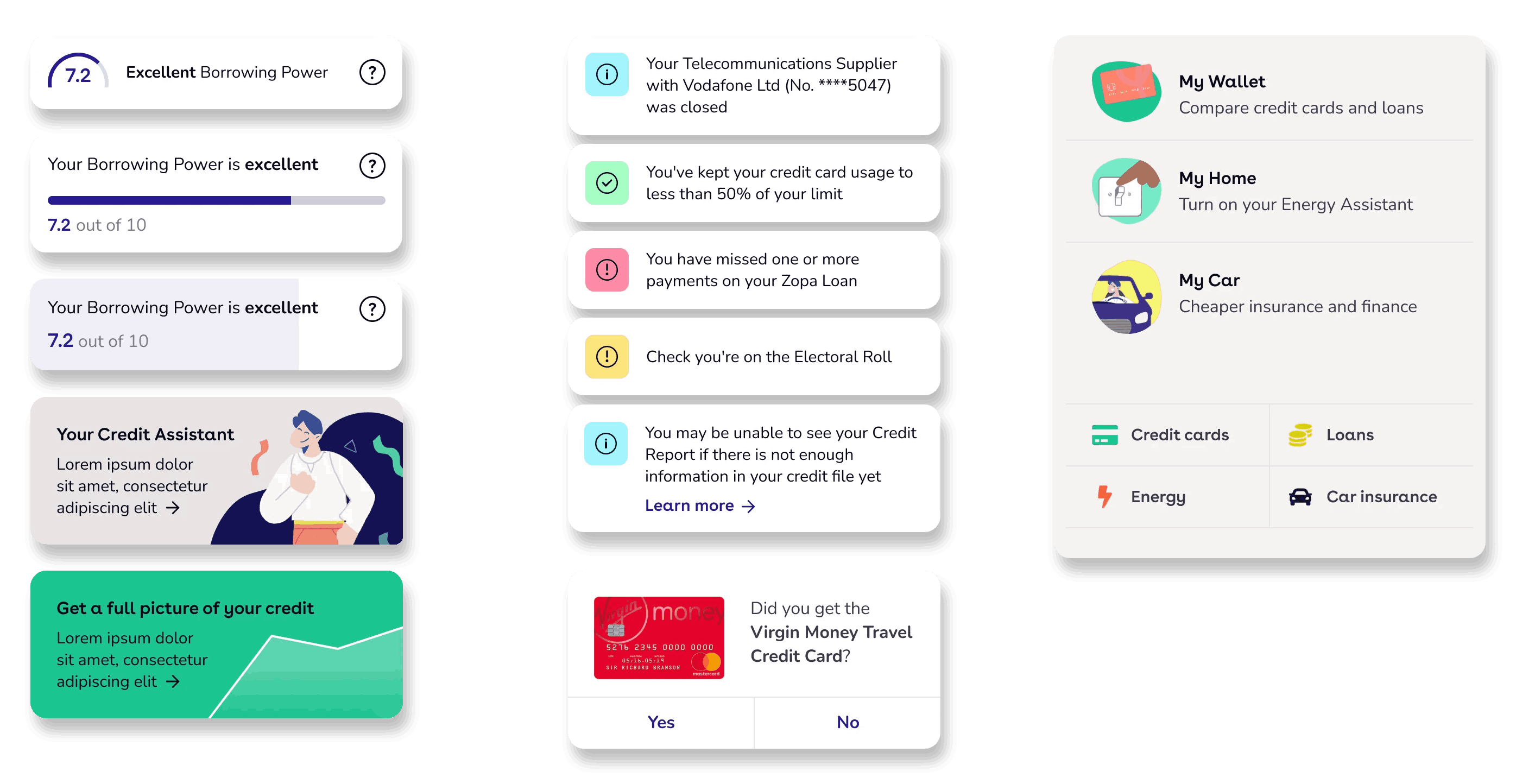

Contextual Alerts for Financial Health Checks

Users valued timely notifications that would help them stay on track with financial plans. Alerts for bills, subscriptions, and spending patterns were proposed to increase retention and trust.

Lack of timely notifications and need for financial health monitoring.

Bud’s technology would support real-time alerts based on spending patterns, upcoming bills, or unusual activity, encouraging users to review and adjust their financial habits.

To gain insights into TotallyMoney's user base, six individuals were interviewed to explore their methods for tracking daily incomes and expenses, as well as their opinions on the current app.

To gain insights into TotallyMoney's user base, six individuals were interviewed to explore their methods for tracking daily incomes and expenses, as well as their opinions on the current app.

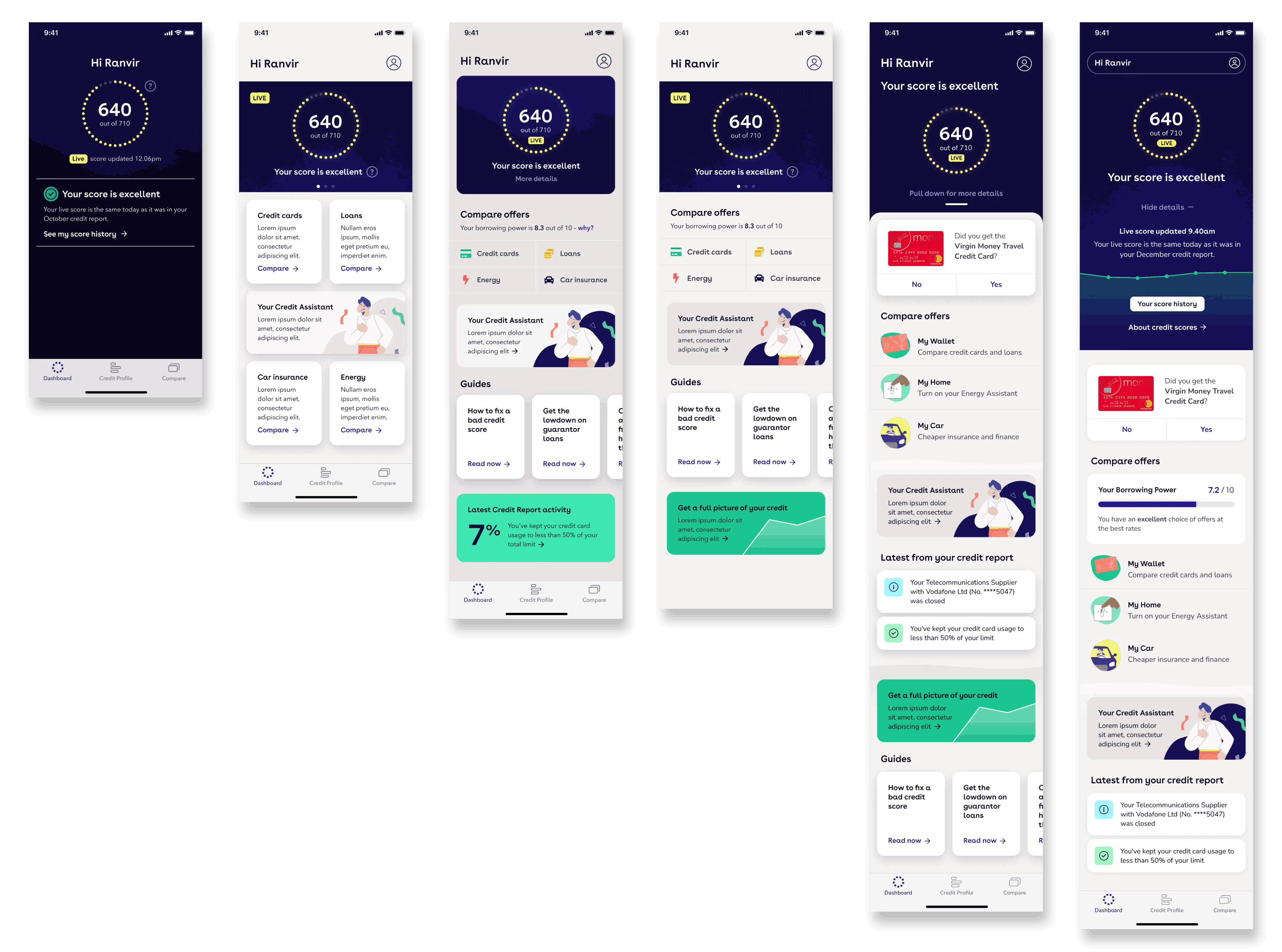

The final designs were developed with consideration of Bud's existing technology, ensuring that TotallyMoney's distinctive branding was seamlessly integrated into its reliable Open Banking framework. Many of the pain points identified during user research had already been addressed within Bud's framework, ensuring a smooth implementation.

The final designs were developed with consideration of Bud's existing technology, ensuring that TotallyMoney's distinctive branding was seamlessly integrated into its reliable Open Banking framework. Many of the pain points identified during user research had already been addressed within Bud's framework, ensuring a smooth implementation.